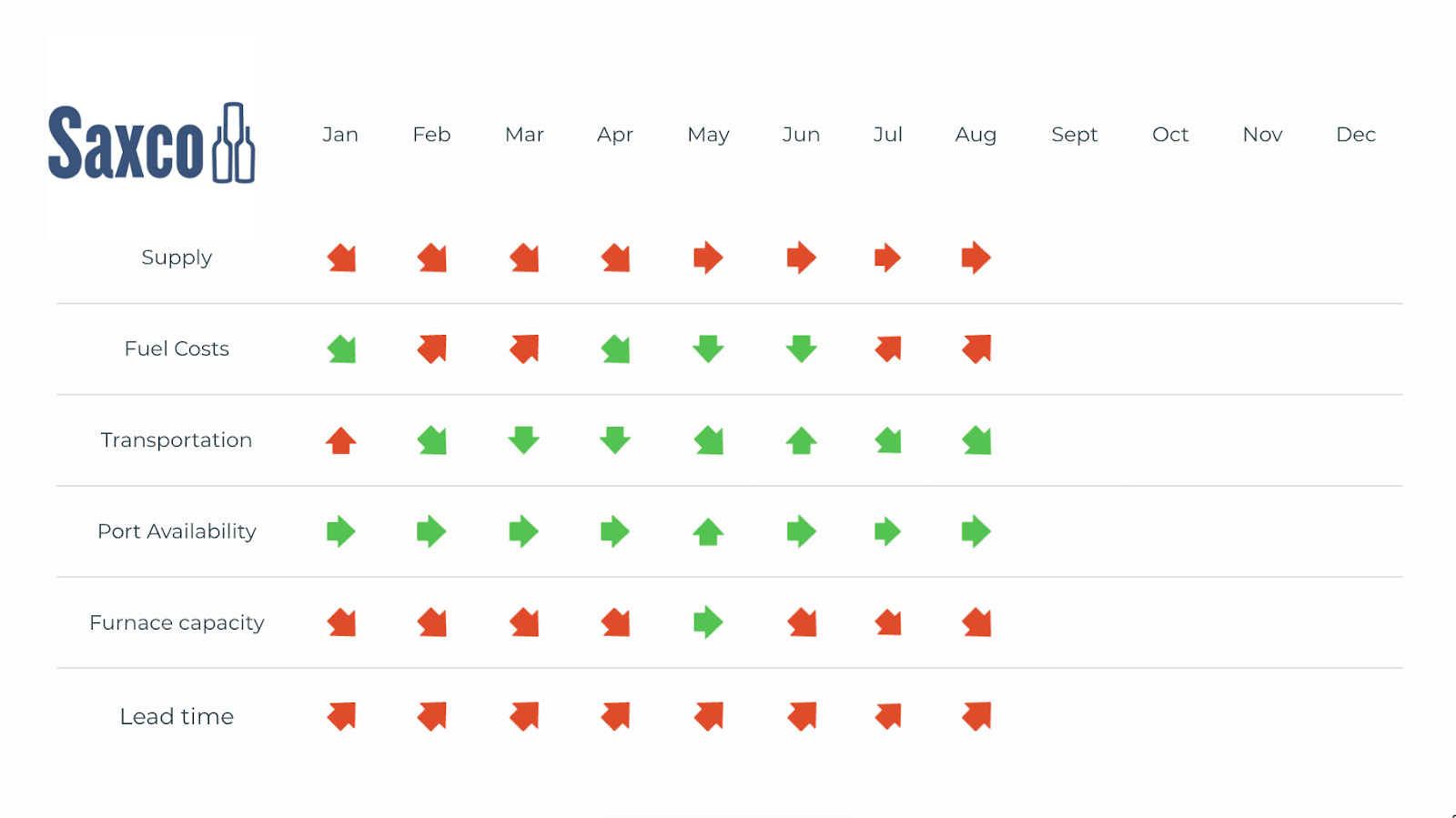

July's supply chain landscape feels deceptively calm, but the undercurrents are shifting. Fuel costs ticked upward again – $3.599 to $3.779 per gallon – putting quiet pressure on logistics, even as transportation costs eased with the surprising disappearance of peak season surcharges. That dip is a welcome but likely temporary reprieve.

On the production side, capacity continues to tighten: OI’s Portland plant has officially closed, and two additional furnaces are scheduled to go offline, which continues to raise concerns about domestic supply heading into the back half of the year. Lead times have not budged from June’s elevated levels, but with fewer furnaces online, we are likely to see that stress compound by fall. Ports remain neutral, and overall supply feels steady – but for now, it is a still surface over increasingly strained infrastructure.

Tariff watch: The rules are changing

The new US tariff rates announced on July 31 mark a significant shift in the trade wind –particularly for glass and wine. EU imports are now subject to a 15% tariff on standard wine bottle sizes (375ml, 750ml, and 1L), a move that will reshape sourcing math for many in our industry. The new rate took hold August 7, but the old rates apply for goods that meet certain “on the water” criteria before August 7 and are entered for consumption before October 5. Still, any attempt to sidestep these costs through transshipment could trigger a brutal 40% penalty tariff, plus potential fines or penalties – no small risk for those trying to outmaneuver the system.

The aggregate US IEEPA tariffs on Indian glass increased to 25% on August 7 and will rise to 50% on August 27, while the aggregate US IEEPA tariffs on Chinese glass are still scheduled to increase from 30% to 54% on August 12 – unless a diplomatic off-ramp appears. In Canada, fentanyl-linked tariffs rose from 25% to 35% this month, though USMCA-origin goods remain safe.

Taken together, this constellation of tariff shifts signals a more complex and costly global market – especially for smaller-format bottles and price-sensitive products. Reports from the EU and New Zealand warn that boutique exporters may be among the hardest hit. For importers and bottlers in the US, strategic recalibration is no longer optional – it is now table stakes.

Consumer pulse: Value, redefined

Consumer behavior is shifting in ways that matter for packaging decisions. Deloitte’s latest numbers show over half of consumers have switched brands recently, but not necessarily to save money – they are chasing better value. There is a difference, and it shows up in purchase patterns. Nearly 40% plan to treat themselves to something small but meaningful this quarter, which keeps premium consumables in play if they justify the spend.

This nuance is especially relevant in categories like premium wine and spirits. Over half of consumers say they have recently switched brands to find better value. Not better pricing – better value. That could mean a more beautiful bottle, a more compelling backstory, or simply a product that feels like a reward. As mentioned, nearly 40% say they plan to indulge in something small but meaningful this quarter, which means there is still oxygen for premium formats – if they speak to the moment.

For glass customers, this is not a race to the bottom. It is an invitation to differentiate. In a value-driven world, quality, story, and detail still win.

Bottled Tidbits – Daylight robbery: The tax that dimmed the world

Before the 17th century, windows were not a structural standard – they were a status symbol. Glass was so rare that when Britain needed to raise funds in 1696, Parliament did not tax income or land. Instead, they taxed windows. It is a fact: homeowners were charged based on the number of glass panes they had. The result? A generation of buildings with bricked-up windows is still visible across parts of Europe today. It was known as a “tax on light and air,” and it is where we get the phrase "daylight robbery”.

Though repealed in 1851, the damage lingered: historical records show glass production between 1810 and 1851 was essentially flat, despite a housing boom. Only with mass manufacturing did both windows and bottles become widespread. Glass was not always everyday. Once upon a time, it was the dividing line between those who could look out and those who could not afford to.

Loading comments...